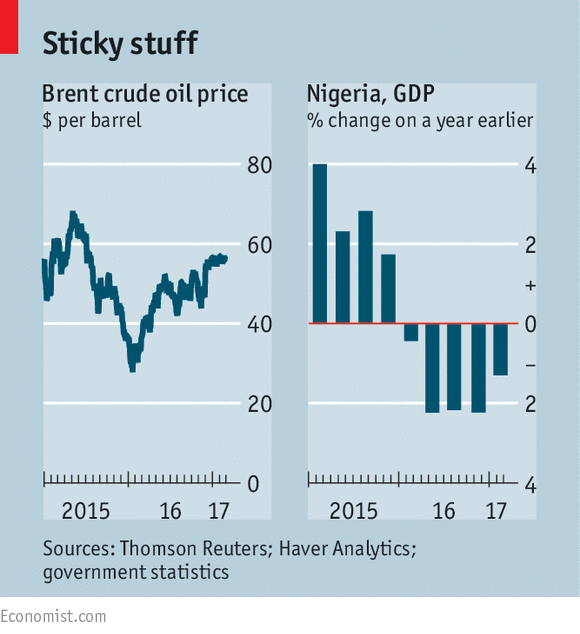

SITTING on the pavement outside the Lagos state government secretariat, Empero flicks through newspapers, looking for jobs. “We are smiling and we are dying,” says the 36-year-old, a town planner by trade. Nigerians are known for their dramatic turn of phrase. But recent events may justify such rhetoric. The economy shrank by 1.5% in 2016. Inflation has more than doubled to 18.7% in 12 months. Meanwhile, the president, Muhammadu Buhari, has been out of the country since January 19th, receiving treatment for an undisclosed illness. There could hardly be a worse time for the 74-year-old former military dictator to be incapacitated. But much of the blame for Nigeria’s current economic troubles can be laid at his door.

Mr Buhari was elected in March 2015 promising to defeat Boko Haram, the jihadist group terrorising the country’s north-east, and to tackle endemic corruption. He had on his side a wave of hope; he was the first Nigerian opposition leader to oust an incumbent peacefully at the ballot box, despite his authoritarian past.

On national security he has made progress: Boko Haram, now splintered into two factions, no longer controls any big towns. But it is far from defeated, as the government has claimed repeatedly in the past couple of years. With many farmers still unable to return safely to their fields, hunger stalks the region: 450,000 children are severely malnourished. Elsewhere, clashes between Muslim Fulani herdsmen and largely Christian farmers in southern Kaduna, in Nigeria’s fractious Middle Belt, have killed at least 200 people since December. Oil production has not fully recovered after money-hungry militants attacked pipelines and rigs in the Niger Delta last year. When it comes to corruption, a number of bigwigs have been arrested and bags of seized money paraded before the media. Yet there have been no high-profile convictions yet. The state may be led by a former strongman, but it is still fundamentally weak.

It is the troubled economy, though, that looms largest now in Africa’s most populous country. Mr Buhari was inaugurated soon after the collapse of global oil prices. But instead of accepting reality (exports and government revenues are dominated by the black stuff), he reverted to policies he implemented when last in power in the 1980s, namely propping up the currency. This has led to shortages of foreign exchange, squeezing imports. The central bank released the naira from its peg of 197-199 to the dollar in June 2016, but panicked when it plunged, pinning it again at around 305. Exchange controls are still draconian. Consequently, many foreign investors have left, rather than wait interminably to repatriate profits. “The country is almost uninvestable,” says one. Importers that can’t get hold of dollars have been crippled. “To take a bad situation and make it worse clearly takes a bit of trying,” says Manji Cheto, an analyst at Teneo Intelligence, part of an American consultancy.

By February 20th the naira had sunk to 520 on the black market. It has since recovered by around 13% after the central bank released dollars and allowed posh Nigerians to buy them cheaply to pay for school fees abroad. The reprieve is likely to be temporary, though. Most analysts agree that the naira should float freely. Egypt, which devalued the pound in November in return for a $12bn IMF bail-out, is an oft-cited example. After falling sharply it found a floor before rebounding as the best performing currency in the world this year. However, Nigerian officials worry that the inevitable inflationary spike could lead to unrest, particularly if they are forced to raise subsidised petrol prices. It is also anathema to Mr Buhari, who is thought to blame an IMF-advised devaluation for the coup that ejected him from power in 1985. “They all know what needs to happen,” says a Western official of the nominally independent central bank’s leadership. “But somehow they don’t dare to [do it].”

The IMF predicts Nigeria’s economy will expand by 0.8% this year. That would lag far behind population growth of around 2.6%. But the government will tout any recovery as a victory. “That’s the real danger, that they will take that as validation their policies are working,” says Nonso Obikili, an economist. Meanwhile, Nigeria continues to take out expensive domestic and foreign loans. While debt remains relatively low as a proportion of GDP, at around 15%, servicing it is eating up a third of government revenues. After a $1bn Eurobond issue was almost eight times oversubscribed last month, it plans to issue another $500m one this year. Officials have also said that they want to borrow at least $1bn from the World Bank. That remains contingent on reform.

If Mr Buhari remains in London much longer, his absence could provide a window for Nigeria’s technocratic vice-president Yemi Osinbajo to push through a proper devaluation. Mr Osinbajo, currently in charge, has proved an energetic antidote to his ponderous boss, visiting the Delta for peace talks and announcing measures intended to boost Nigeria’s position in the World Bank’s Ease of Doing Business rankings, in which it currently ranks a lowly 169 out of 190.

Mr Buhari called the governor of Kano during a prayer meeting on February 23rd to say he was feeling better, the first time Nigerians had heard from their president since he left the country. But the state of his health is still unclear (aides have said only that he needs more rest). Mr Osinbajo’s appointment as acting president has followed constitutional protocol. In 2010, by contrast, it took three months for Goodluck Jonathan, a southerner, to be cleared to rule while Umaru Musa Yar’Adua, the northern president, lay dying in Saudi Arabia. There are ghosts of that power struggle in rumours that Mr Buhari’s closest allies are manoeuvring to try to keep the presidency with a northerner should their boss die or be forced by ill health to step down. That could split the ruling All Progressives Congress into three or four factions, destabilising policy-making. Nigeria’s best chance of reform in the short run, then, is probably for the president to rest up in London a while longer.

Be the first to comment